Soaring home prices and the perceived lack of available stock have dulled the mood among many buyers in the past three months, although sentiment has lifted to a record high for existing homeowners who are now feeling wealthier and more confident about their finances, an industry survey shows.

16 Comments

The year of 2020 is likely going to be remembered as one of the most interesting and eventful years of an entire generations’ lives, across a number of areas, not least of which is investing. Financial markets have unsurprisingly taken a hit, however with circumstances resembling nothing the world has ever seen before, that hit has been followed up with what some analysts have defined as irrational. The trickle on effect is now spreading to other areas of the economy, with some analysts suggesting property may be next, but things are not quite as grim as some have forecast, with more realistic scenarios seeing property markets take a mild dip, paving way for a new generation of successful investors in Australia's millionaire maker market.  Following a record breaking 38% dive following the outbreak of COVID, we’ve seen share markets make surprising bounce backs and follow-on drops, entire exchange indexes display the characteristics of small cap shares, oil prices drop below $0 for the first time in history, airlines go bust, unemployment rates skyrocket and entire industries become all but redundant. Amidst the chaos, real estate, the bedrock of Australian investing, has managed to remain relatively unaffected. Whilst property markets have seen considerable reductions in sales and listing volumes, and auction clearance rates have spiked up to 65% in some major cities, the asking price for those who are listing has dropped just 0.9% and 0.2% in Sydney and Melbourne respectively from March to April. The sentiment in Brisbane has even improved, with a median ask price increase of 0.7%, showing that Aussie homeowners still have a lot of confidence in the market. Nevertheless, this situation is now at a stage where the entire economy is being affected, and It would be unwise to assume that property is completely immune. The strength of property markets to date has attracted the attention of leading economists and analysts over the past month and there appears to be little doubts that a real estate market hit is imminent. How large, which areas and regions will be affected most, and for how long the downturn is to last vary from report to report, but one thing is consistent: a dip is coming. However, whilst there are some more pessimistic forecasts doing the rounds in the media, we see this drop realistically being less severe, easily recoverable, and therefore presenting some of the best opportunities in property investing for a generation.  What are “they” saying? There are mixed predictions on house price changes. In a review of the effect of unemployment rate rises, AMP Capital chief economist Shane Oliver suggested that in a best case scenario capital cities would see a 5 percent price decline, and in a worst case scenario, that number could be as much as 20 percent. Meanwhile, a recent report from CBA has forecast a median house price drop of 10% within the next 6 months, which seems to be a figure that many analysts are agreeing with. Some analysts are anticipating more serious changes, though. SQM Research founder Louis Christopher reported to ABC’s The Business that if a second wave of coronavirus hits, we are likely to see a “major fall” in prices. "When I say major we're talking up to a 30 per cent decline over a 12-month period, with the bulk of those declines occurring in Sydney and Melbourne," he said. This may seem a bit doom and gloom, however it is important to note that these predictions are largely hinged on variables that still remain quite unpredictable and, in some cases, not very likely. The economic effect of this pandemic is already in motion to impact Australian property markets, so some impact is now all but inevitable, but the more pessimistic outlooks are based on the pandemic getting substantially worse, and so far Australia’s response has proven effective, with many restrictions easing. Whilst we can expect a drop, it is perhaps unrealistic to expect the worst of these outlooks to come to fruition.  Key factors to watch: With this kind of uncertainty, knowing what to look out for is imperative. The best approach for this is to work with a professional, and Buyers Club consultants are the best in the game, keeping our members in the know on the changing investment landscape. Whether you are a member or not, here are a few of the key factors to look for when considering these property market forecasts: Coronavirus itself: the magic number here is known as the COVID-19 Growth Factor, and it is calculated simply by taking today’s new cases and dividing it by yesterday's new cases. if this number is above 1 then the pandemic is worsening, and if it is below 1, we’re heading in the right direction. Our current growth factor as at May 20th is 0.98, and with low numbers of new cases this is a comforting statistic. Our highest growth factor was on March 18th where we hit 1.28. Latest outlook: Australia’s restrictions have continued to ease and our progress out of the pandemic is looking more promising than slipping backwards at this point...as long as we can all behave ourselves. Unemployment rates: April saw some alarming increases in the unemployment rate, which has an effect on all areas of the economy. Current unemployment rate estimates for May are sitting around 7%, however there is a risk that this figure could be much higher. Analysts suggest that if unemployment reaches double figures, a much more serious and widespread economic downturn could occur, and the anticipated “V” shaped recovery may not be possible. Latest outlook: April’s reported unemployment rate hit 6.2% which is a substantial increase, however we are still a long way from double digits, and with restrictions easing allowing many businesses to get back to work, this is more likely to flatten than spike again. Mortgage holiday endings: perhaps the best test the real estate market will face is the removal of mortgage holiday periods. In the face of unemployment rises and credit defaults, many Australian banks offered loan repayment pauses, allowing borrowers to temporarily stop paying their mortgage. However this is not removing the debt, it is simply postponing it. At some point, these mortgage holidays will end, and if this is timed with some other factor negatively impacting factors it may be the trigger for vendors to drop their asking prices. Latest outlook: Australia’s household debt-to-income ratio of almost 200 per cent, the bulk of this being mortgages, and is one of the largest in the world, so that isn’t promising. However we also have a property supportive government, and between state and federal governments new initiatives to soften the adjustment are being proposed each week.  There is opportunity awaiting for those who are prepared.

With all this uncertainty, it can seem a bit difficult to know exactly what to do. To this end, we refer you to one of the greatest investors of our time, Warren Buffet, who famously quoted: “Be Fearful When Others Are Greedy and Greedy When Others Are Fearful”. Right now there is a lot of fear in Australian property markets, and this creates opportunities for those who can see it, or more-so, those who are prepared and have a plan. It is imperative that you have a well thought out strategy in place for capitalising on the changes set to occur. Being reactive in a changing market is dangerous and could land you in hot water as a result of rushed decisions. Buyers Club members have access to experienced and professional property investing consultants, who are committed to helping each and every member put together an effective and market relevant plan. Having a buyers agent has never been more important than now, with adjustments to rental yields from price drops, growth area changes as work and lifestyle shifts bring people into their homes more, and an increased demand for reliability and affordability in the wake of uncertainty. You can put yourself in the best position to be greedy while the rest of the market is fearful, and realise investment returns not possible in a more straightforward and steady market, but it cannot happen with the right preparation and planning, and the time for that is now. Become a member today and our Buyers Club consultants will work with you to strategise, plan and prepare for the right investment at the right time.  As COVID-19 has spread around the globe, governments and authorities have been forced to take drastic measures in order to respond to the outbreak, keep people safe, and attempt to safeguard their economies for the future. The virus has had an unprecedented and long-lasting effect on the lives of countless people and its economical effects will also be felt for many years to come, with the Australian share markets seeing their worst declines since the days of the Great Depression. It's only natural that people all over the country, especially investors, are feeling the unique levels of strain and pressure induced by such a traumatic and previously unheard of situation. Property Retains StabilityInterestingly enough, however, while shares have collapsed, the nation's housing market has remained relatively stable during this period of crisis, without a great deal of disruption, suggesting that property investors may not have such great need to fear, after all. While the All Ordinaries Index has been dropping like a stone, residential property investment suddenly seems safer and more secure than ever before. Property investment has always been regarded as a safe choice, particularly as the values of houses and other forms of property only ever seem to rise, and this 'safety factor' is attracting more and more shrewd investors towards residential properties as this turbulent time.  Rising Levels of InterestWhile many investors around Australia may feel uneasy during this time, others are seeing it is a money-making opportunity. As history has taught us, a lot of money can be made even in the most difficult of times. As more and more people sell off their shares and seek to invest their capital in more secure and stable assets, the interest in residential investment is rising, with low-interest rates and relative market stability just a couple of key property-specific advantages appealing to shrewd investors around the nation. Bouncing BackOf course, the market will feel some minor knock-on effects due to the major economic shift induced by the pandemic as overall economic growth begins to decline and homeowner confidence temporarily decreases, but if there's one thing we've seen time and time again from the property market in Australia, it's that it always bounces back. Even as recently as 2019, when experts were predicting major home price crashes in the subsequent months, housing remained strong, the Sydney and Melbourne markets exploded, and sensible investors enjoyed favourable returns on their investments. Future IncentivesMortgage repayment relief, stamp duty reduction, and incentives for first-time buyers are just a few possible incentives the government may introduce to stimulate housing market growth and save the market from a catastrophic crash. With these aids in place, the resilience, resistance, and fortitude of the property market will shine through once more. Buyers Club members have access to the best support and advice available in real estate investing. We can help you to not only last the down market, but thrive in it and come out the other side not just secure, but profitable and with a boosted portfolio ready for growth.   Dear Buyers Club Members, These are unprecedented and challenging times, and we would first like to wish you and your loved ones well. We recognize the seriousness of the COVID-19 pandemic and sincerely hope that all of our customers will remain safe and in good health during this time. We also wanted to let you know how Buyers Club is dealing with the current challenges and what you can expect from us moving forwards. Clients can rest assured that our doors will be remaining open and business will continue as usual, as we endeavour to provide all of our members with the same high standards of service they have come to expect of us. As a forward-thinking business, Buyers Club has always had an adaptable, flexible nature, ready to cope with changing circumstances and seamlessly adjust to new situations, allowing us to continue working through the crisis without any noticeable disturbances. Our state-of-the-art digital systems allow our workers to operate effectively and efficiently from safe, remote locations in their own homes, while the core elements of our work, including online research and analytics, remain unaffected by this pandemic, letting us continue finding the best deals for our members. HOW WE ARE WORKING THROUGH THISWhile the vast majority of our business operation has been untouched by COVID-19, we have had to make some changes and take some precautions in order to protect our workforce:

OUR COMMITMENT TO YOUThese essential adjustments have been made in order to preserve and protect the health of our staff, as well as our valued clients, but our commitment and dedication remain steadfast and unaffected in this time of crisis. In the weeks to come, we will provide additional, current market-specific content and articles that can help you make the right investment decisions during this time. While the current crisis may evoke some fears and doubts around investing, it can prove to be a valuable opportunity for those with a sound strategy. Our expert consultants are working to ensure the strategies we develop and the investment deals we source are the very best the market has to offer. We acknowledge the uncertainty and we also recognise that your membership is a valuable investment in yourself and your future, and we are committed to ensuring that investment pays off. OPPORTUNITIES IN THE MARKETInvesting during a down market ultimately leads to the biggest long-term yields, and this is actually one of the best possible times to join Buyers Club and learn how to build your property portfolio for the long term. As Warren Buffet himself once said, “Be fearful when others are greedy, and greedy when others are fearful”. Get in touch with a Buyers Club consultant today to learn more about how you could be making money and investing smartly in the current market, and stay tuned for more information and advice on property investments in the coming weeks.  The rebound in property prices has made households more upbeat about the prospect of further capital gains, with both owner-occupiers and investors revising up their price expectations for 2020.

Property market sentiment has rebounded sharply among investors but first home buyers are starting to feel the pinch of affordability pressures, the latest ME Quarterly Property Sentiment Report shows.

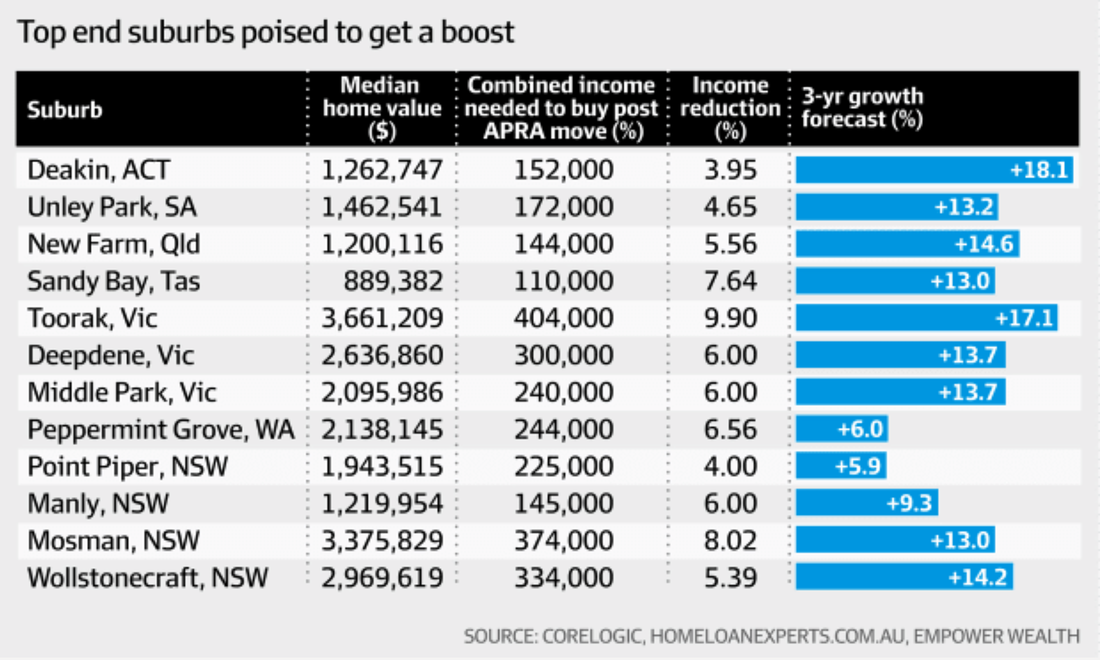

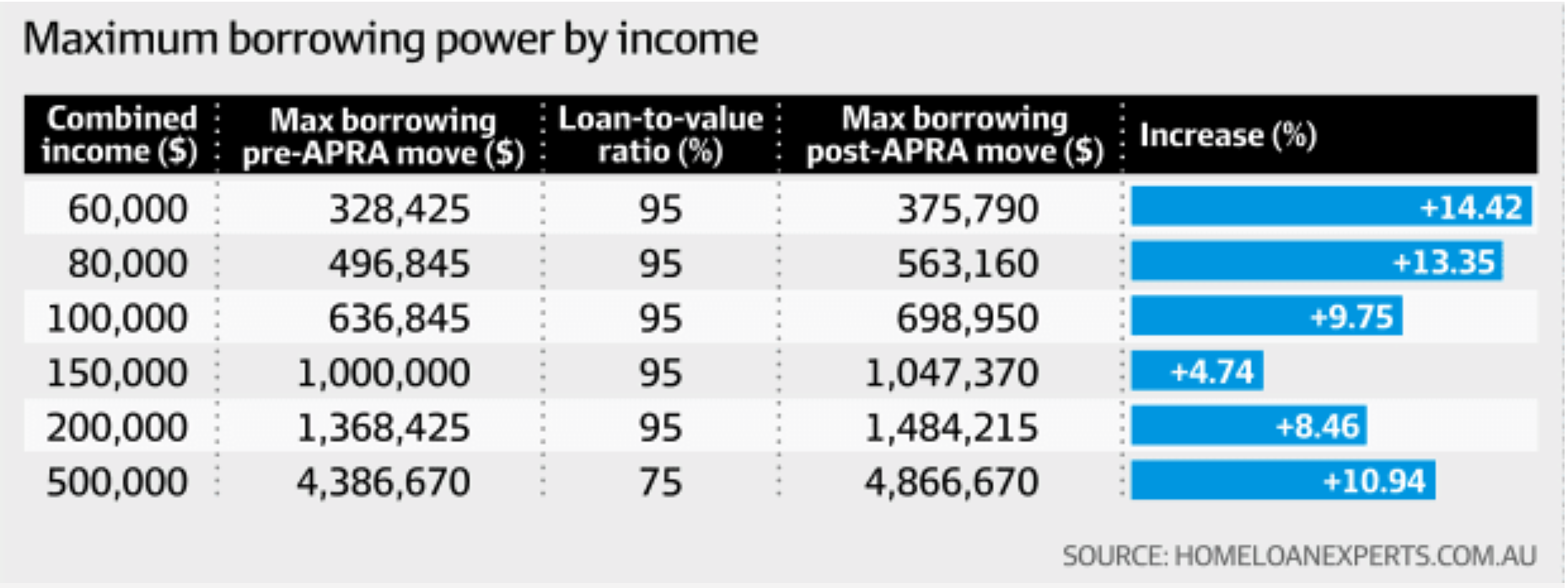

A national poll of 1000 investors, owner-occupiers and first home buyers at the start of October found that confidence improved dramatically over the past three months, fuelled by the consistently strong price growth across major markets and signs that banks were lending again. Forty-two per cent of Australians were feeling upbeat about the property market – up by 9 per cent compared to the previous quarter. While sentiment improved across every age group, property status and buying intention, investors and Millenials and those who plan to buy in the next 12 months were the most optimistic. n contrast, sentiment among first home buyers has been subdued as affordability constraints started to bite, ME’s general manager for home loans Andrew Bartolo noted. ‘‘One of the flow-on impacts of increased sentiment has been price increases. This impacts the first time (buyer) more acutely than investors whom they are competing with,’’ he said. Almost half (47 per cent) of those surveyed expect prices to rise over the next 12 months, up from 38 per cent in July. Sydney-based buyers’ agent Samara Metri, director of Buyers Club, said the business was signing twice as many clients per month as it was a year ago. ‘‘This time last year we were signing up around 10 clients a month, now we’re adding between 20 and 25 clients,’’ Ms Metri said. ‘‘We’ve not only had more people come on board but they’re transacting much faster. ‘‘We’ve even noticed a lot of competition when negotiating on property as real estate agents are becoming more confident.’’ Scott O’Neill, director of Rethink Investing, said investors have returned to the market in a big way. ‘‘We’re literally twice as busy now compared to this time last year. The negative sentiment has been lifted,’’ he said. Mortgage brokers have noticed a rise in the number of people applying for a loan since the federal election. ‘‘This could be attributed to pent-up demand from buyers who had put their purchasing plans on hold and now want to take advantage of the low interest rate environment,’’ said Mortgage Choice chief executive officer Susan Mitchell. Original article published in the AFR. Nov 2019.  Aspirational suburbs are poised to get a boost as buyers who were previously priced out of the market are now starting to trickle back armed with more confidence and bigger budgets. Thanks to the prudential regulator's decision to allow banks to reduce their affordability buffers in assessing borrowers, buyers can now borrow up to 20 per cent more depending on their situation. Sharon Xie, credit manager of Homeloanexperts.com.au estimates a couple with a combined income of $200,000 (no dependents and standard living expenses) can borrow an additional $115,790 under the new assessment rate, increasing their borrowing power from $1,368,425 to $1,484,215. It may be early days, but there are signs that the upper end of the market is already responding to this stimulus. Corelogic's senior research analyst Cameron Kusher said that while the upper end of the housing market has seen some of the largest declines during this downturn– Peppermint Grove, in Perth, plunged 18.7 per cent over the past 12 months, Brisbane's New Farm sank 23 per cent and Sydney's Mosman dropped by 10.1 per cent – the segment as a whole has shown the strongest improvement over recent months. "The top end of the market has fallen by 0.3 per cent over the past three months compared to a 0.6 per cent drop across the most affordable 25 per cent of the market," Mr Kusher said.  "The adjustment to serviceability limits, the removal of this limit and the change to a 2.5 per cent buffer mean people that were in a position to already get a mortgage can potentially now borrow more. With higher valued properties having recorded the largest value falls, owners looking to upgrade may now be looking to buy." "The adjustment to serviceability limits, the removal of this limit and the change to a 2.5 per cent buffer mean people that were in a position to already get a mortgage can potentially now borrow more. With higher valued properties having recorded the largest value falls, owners looking to upgrade may now be looking to buy." Sydney buyer Dr Steve Hou is among the growing number of upgraders who are taking advantage of lower interest rates and increased borrowing power. He and his family recently splashed out on a free-standing home in Bellevue Hill, paying $3,480,000 at a heated auction. “It was crazy. Everyone was bidding confidently so I was pushed to a position where I have to place the highest bid just to win this property. It’s not really good for me [having to pay more] but that’s the way it is,” he said. “We didn’t have our home loan approved for the other property we wanted to buy, so we missed out. This time we got it so we were able to buy this home." Jeremy Sheppard, head of research at Empower Wealth predicts that competition and low stock will continue to drive prices higher over the next three years. "Demand and supply indicators points to a stronger performance in these areas with houses in Toorak set to rise by 17.1 per cent, Wollstonecraft house price to grow by 14.2 per cent and Mosman by 13 per cent," he said. Mr Sheppard's calculation is based on housing indicators like vacancy rates, auction clearance rates, days on markets, vendor discounting and 12 other factors. The broader market is already showing signs of recovery with Sydney and Melbourne recording positive growth in July for the second month in a row after suffering almost two years of price falls. The extra borrowing is also a big deal for investors who were hammered by the strict lending policies over the past couple of years. It allowed Sydney-based first-time investors Ashleigh Digby and her partner Dylan Holmes to buy a bigger property in Queensland. "The lower assessment rate has increased the amount we could borrow and gave us more options," Ms Digby said. "It took away a lot of restrictions on what we could buy." The $349,000 property the couple bought was out of reach when they first started looking three months earlier. "We were initially going to buy a single key property because we were short by $50,000 to buy a dual key home. After the [Australian Prudential Regulation Authority] move, we were able to borrow an extra $70,000 and 'upgrade' to the bigger investment property instantly. "We want to build our portfolio in the next five to 10 years. This just made it easier for us to get started."  Investors who were trapped in their mortgage are also being given a lifeline according to Justin Picker, property investor and mortgage broker with Picker Financial Solution.

"Property investors who were stuck in their mortgages due to servicing limit can now look to refinance if they qualify," he said. "This would allow them to continue to buy more investment properties and grow their portfolio." But while the banks have dropped their assessment rates, this doesn't mean that it's now easier to get a mortgage. "The banks are still strict with their lending and it still takes time to get loans approved," Ms Xie said. "They're scrutinising each loan application and combing through the applicant's transaction and credit card statements to analyse the expenditure of the household. "If you want to improve the chances of getting a loan approved consider cutting down on unnecessary financial commitments or personal spending," she said.

|

- 1300 505 605

-

Sydney: Unit 311/2-8 Brookhollow Ave, Baulkham Hills NSW 2153

Melbourne: Chadstone Tower 1 - Level 8, 1341 Dandenong Road Chadstone VIC 3148

RSS Feed

RSS Feed